Choosing Between a 401(k) and IRA in 2026

Your Complete Guide to 401(k) and IRA Changes for 2026

What’s New for 2026

- The Internal Revenue Service (IRS) issued its annual inflation adjustment under Notice 2025-67, which means higher contribution limits for 401(k), IRA, and other retirement plans. (Source: KMPG)

- Under SECURE 2.0, new rules begin in 2026 requiring that catch-up contributions made by certain higher-income participants be designated as after-tax Roth contributions and increasing catch-up contribution limits for certain retirement plan participants, in particular employees between the ages of 60 and 63 and employees in newly established SIMPLE plans. (Source: IRS)

With those changes, here’s how 2026 compares—and how you can decide what works best for you.

Updated 2026 Contribution Limits & Catch-Up Rules

The 2026 increase gives savers a little more flexibility—especially those catching up near retirement—but also introduces important tax-treatment changes that matter for decision-making.

Tax Treatment & SECURE 2.0: New Roth Catch-up Rule

Traditional vs. Roth: What’s the difference?

- Traditional 401(k)/Traditional IRA: Contributions are pre-tax; withdrawals are taxed later.

- Roth (IRA or 401(k) where allowed): Contributions are made with after-tax dollars; qualified withdrawals are tax-free.

What’s new under SECURE 2.0 for 2026

- Starting in 2026, if you are age 50 or older and your prior-year wages from the same employer exceeded $145,000 (indexed annually), then any catch-up contributions must be made to a Roth 401(k)—i.e., after-tax.

- This applies to 401(k), 403(b), or governmental 457(b) plans. If your employer plan does not offer a Roth option, you may not be allowed to make catch-up contributions under the new rule.

Implication: For high-earning older workers, catch-up contributions become after-tax, which alters the traditional tradeoff between current-year tax deduction and future withdrawals.

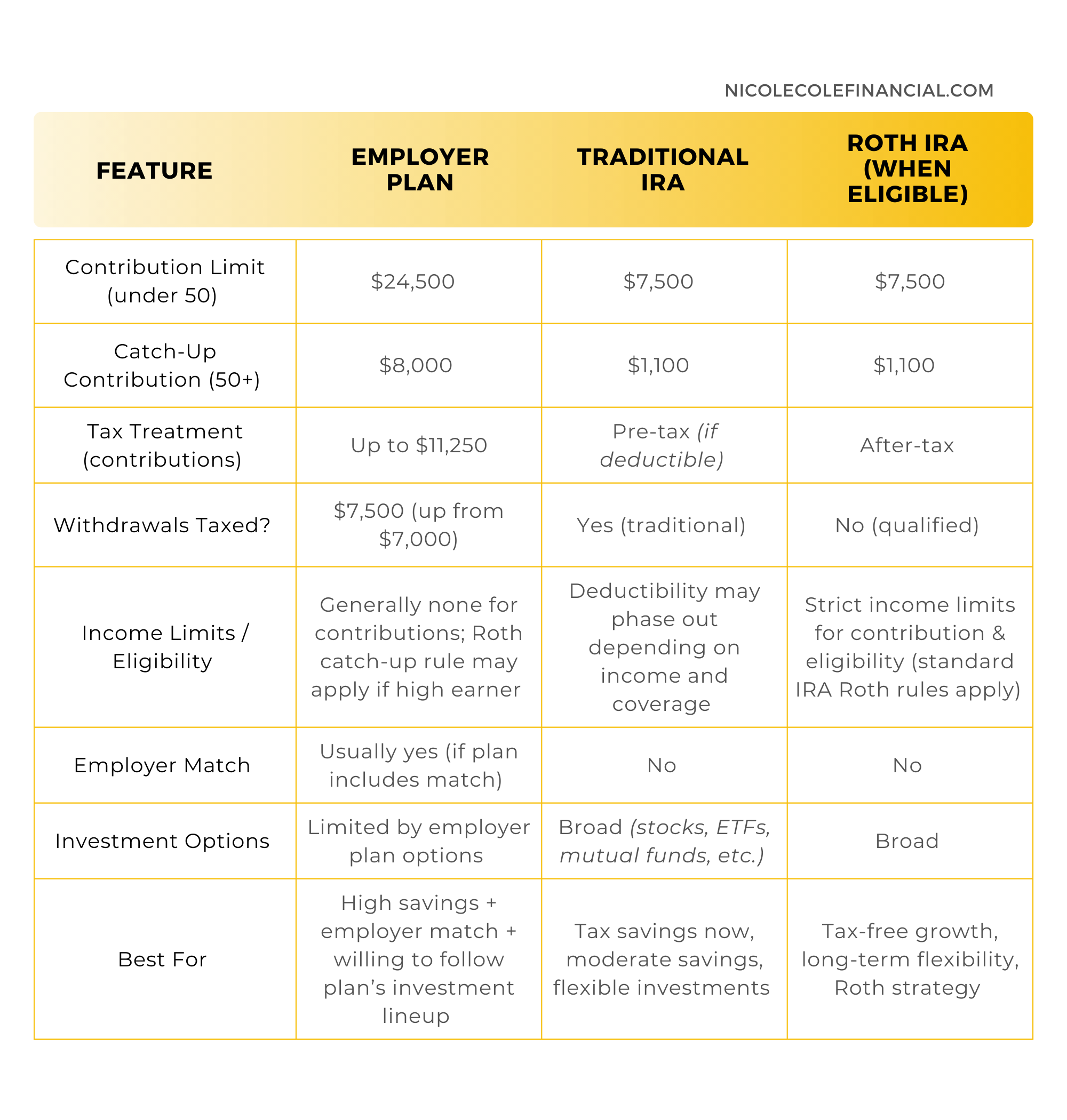

2026 401(k) vs. IRA: Updated Comparison Table

Who Should Use Which And When a Mix Makes Sense

- If your employer offers a match, max that out—it’s “free money.”

- If you expect your retirement tax rate to be higher than now, a Roth (IRA or 401(k)) might make sense.

- If you’re over 50 (or nearing 60–63) and want to maximize savings, take advantage of catch-up (or super catch-up) provisions.

- If you want investment flexibility, IRAs give far more choice than typical employer plans.

- For high earners, be aware: catch-up in 2026 may be after-tax due to the SECURE 2.0 Roth requirement.

Many people benefit from using both—contributing to a 401(k) (for match or high deferral limit) and an IRA (for tax flexibility or investment choice).

What’s Changed Since 2025 And Why It Matters

- Higher contribution limits—both for 401(k)s and IRAs. This means more opportunity to save.

- Mandatory Roth catch-up for some high earners (2026)—changes the tax tradeoffs for older, high-income savers.

- Super catch-up remains for ages 60–63—giving older savers extra room.

- Investment flexibility and tax planning are growing in importance—with evolving rules, combinations of Roth, traditional, 401(k), and IRA may yield the best long-term results.

Final Thoughts

There’s no one-size-fits-all answer. The “right” retirement vehicle depends on your income, tax bracket, age, and how you view taxes now versus later.

With 2026 bringing higher limits and new rules under SECURE 2.0, now is a great time to review—or build—a retirement strategy that works for you.

The key: stay flexible, stay informed, and adapt as the rules evolve.

Ready to align your 2026 retirement plan with your long-term goals?

Let’s build a strategy together that maximizes your savings potential—while navigating the new 2026 rules.

Take control of your retirement plan.

Resources

Notice 2025-67: Increased retirement plan contribution limits for 2026, KMPG

2026 401(k) Contribution Limits Issued by the IRS, ASPPA

SECURE Act 2.0: IRS Issues Final Regulations on Catch-Up Contributions, Gould+Ratner

401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500, IRS

*This content is developed from sources believed to be providing accurate information. The information provided is not written or intended as tax or legal advice and may not be relied on for purposes of avoiding any Federal tax penalties. Individuals are encouraged to seek advice from their own tax or legal counsel. Individuals involved in the estate planning process should work with an estate planning team, including their own personal legal or tax counsel. Neither the information presented nor any opinion expressed constitutes a representation by us of a specific investment or the purchase or sale of any securities. Asset allocation and diversification do not ensure a profit or protect against loss in declining markets. This material was developed and produced by Advisor Websites to provide information on a topic that may be of interest. Copyright 2026 Advisor Websites.